In this life, some things just don’t go together.

Orange juice and breakfast cereal. Not in the same bowl, thank you. However, as the commercials during my Saturday morning cartoons taught me, both are part of a “balanced breakfast.”

Stocks and cryptocurrencies? Well, yes – for some long-term investors looking to maximize their growth potential, both might belong in the same diversified portfolio. But not if you’re going to treat them the same way.

Look, I’m not going to tell you how you should invest your money. I am, however, going to tell you about something the Securities and Exchange Commission has been exploring: A framework that could allow some publicly-traded assets to transact in tokenized form on blockchain-based systems.

Now, assets can share similar technology without serving the same purpose. The commodities exchange COMEX sells gold bullion futures side-by-side with interest rate contracts and foreign currency swaps. One platform, one technology with very different investment options.

That distinction matters now because regulators are exploring ways for traditional assets to trade on blockchain-based systems – in some ways, more like crypto. Here’s what’s changing…

The SEC’s plan

Before getting into the details, it may be useful to go over some of the differences between cryptocurrencies and other assets, beyond just the names.

Different asset classes perform differently, and each has its own purpose and function in a diversified portfolio.

A stock (or share, or “equity” generally) typically represents a fractional ownership stake in a corporation. Depending on the type of share, investors may have voting rights. Some companies pay dividends. The price of a stock is tied to the business, its earnings, investor expectations and broader market conditions.

Crypto assets are different. They rarely represent ownership in a company. Depending on the asset, they may function as a decentralized network asset (ether), a medium of exchange (DAI), a store-of-value candidate (bitcoin), a utility token (chainlink), a DeFi protocol token (Aave) or another type of digital asset. Their price is usually driven by adoption, supply-and-demand dynamics, network activity, market sentiment and broader economic conditions.

The major difference, of course, is on the regulatory side. Traditional assets are part of a well-established set of laws and regulatory bodies.

Traditional assets are typically bought and sold through brokerages and market intermediaries, with ownership tracked through a network of clearinghouses, transfer agents etc.

Crypto, by contrast, was designed to allow digital assets to move across decentralized networks. Depending on how an investor holds crypto, ownership and custody can look very different from a traditional brokerage account.

Long story short, the question of ownership with traditional assets is a lot more complicated than with crypto.

But that might be about to change.

Coindesk tells us the SEC is preparing an “innovation exemption” for tokenized securities in the near future:

Major Wall Street players like DTCC, Nasdaq and NYSE unveiled plans to roll out infrastructure for tokenized securities as blockchain increasingly overlaps with crypto.

So why does this matter?

“Tokenization” means expressing ownership of an asset as a digital token on blockchain. I think of it as a digital receipt that anyone can see declaring my ownership of a specific asset. Tokenization would create a permanent, immutable record of ownership and transactions on blockchain.

In traditional finance, ownership records are maintained through market intermediaries. For example, many investors find it strange when they learn that a single company, Cede & Co. is the record owner of over $87 trillion in securities via its subsidiary, the Depository Trust Company (DTC). This sounds nefarious (and a lot of GameStop enthusiasts have conspiracy theories about it), but it’s really just a means of simplifying bookkeeping.

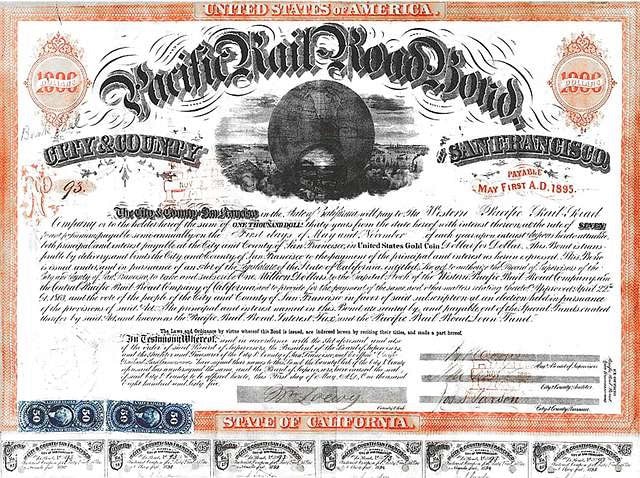

Back in ye olden times, when you wanted to trade a stock, you had to take the physical certificate to your broker. Bonds were ornate certificates, too, and actually had a number of little stamps or “coupons” you were supposed to cut out with scissors and redeem for your interest payments. (In fact, bond yields are still often referred to as “coupons.)

San Francisco Pacific Railroad Bond, 1865. Note coupons at bottom. Public domain image via The Cooper Collection of U.S. Railroad History.

Now, obviously, such a system doesn’t scale very well! Finding and carrying certificates and coupons to a broker who then had to mail them to someone else, well, it was a hassle. Physical certificates did solve the ownership issue handily. Until it was time to transact. Trades settled on a T + 5 schedule (five business days after the trade date).

That’s why, in 1973, DTC was established. It stood at the center of the U.S. financial market, providing clearing, settlement, trade and ownership reporting to all participants in financial markets. Instead of keeping your stock and bond certificates in a floor safe or a safe deposit box at the bank, you could send them to DTC who would confirm your ownership and, presumably, destroy the certificates. Ownership was tracked in a central ledger, later a spreadsheet. This finally allowed trades to settle on the next business day, T + 1.

Tokenization allows blockchain-powered settlement to happen lightning fast, in mere seconds, according to Chainlink.

Clearly, that’s an improvement!

No wonder why the SEC is interested in tokenized trades. We’ve already seen how fast and efficient blockchain-based repo market trading is, why not expand it?

Well, I for one have a few concerns…

What’s wrong with tokenization?

Here’s my first concern: the tokenization process might be in the hand of third parties. (As in not you, the owner, and not the company that issued the security). A middleman could tokenize a share without the issuer’s consent or cooperation.

That’s strange. According to a recent Moneywise article by Aditi Ganguly, CEO of Citadel Securities Ken Griffin worried:

“While the rules governing the national market system can continue to be finetuned, facilitating the emergency of a “shadow” U.S. equity market … would allow tokenized U.S. equities to trade completely outside of the national market system, fragmenting liquidity and undermining core investor protections.”

Ganguly cites Daniel Labovitz, an exchange CEO, who explained: “When the same security trades in different markets that aren’t connected to each other, the price of assets can diverge, meaning that some buyers will overpay” for their asset.

To some degree, we already see this across crypto exchanges. Less liquid exchanges that have fewer transactions happening might have “stale” or outdated prices. Griffin and Labovitz seem concerned that decentralizing trading through tokenization might actually make prices less accurate.

But Labovitz had a more serious concern:

“The tokens may not represent actual ownership of the company, and token holders may not get all the benefits of the share.”

Now, that’s really strange! This idea is not entirely foreign to traditional finance. American Depositary Receipts (ADRs) already let U.S. investors buy securities that represent shares of non-U.S. companies held by a depositary bank. ADRs can make foreign stocks easier to access. But investors still need to understand exactly what they own, what rights come with it and how closely it tracks the underlying shares.

Labovitz is pointing out that tokenized stocks raise a similar question in a newer form: Does the token represent direct ownership of an asset? Or is it just a wrapper that provides economic exposure to price fluctuations, without all the rights of ordinary shares?

Okay – tokenization definitely brings faster trading and settlement. But it’s not all roses, either – tokenization could open the door to fragmentation across trading platforms. Worse still, to uncertainty about what exactly it is an investor just purchased.

The bigger problem: The technology doesn’t change the asset

Tokenization may change how an asset trades. It may change how ownership is recorded. It may even change how quickly a transaction settles.

But it does not change what the asset is.

That’s the key distinction investors should keep in mind. A tokenized stock is still connected to a company. Its value is still tied to that company’s earnings, leadership, competitive position, investor expectations and the broader stock market. Even if it trades around the clock on blockchain-based rails, the underlying exposure is still equity exposure.

Crypto is different.

Most cryptocurrencies do not represent ownership in a business. They are tied to digital networks, decentralized infrastructure, adoption trends, supply-and-demand dynamics, market sentiment and, in some cases, scarcity models or specific utility within a blockchain ecosystem.

That does not make crypto “better” than stocks. It makes it different.

And different is exactly the point of diversification.

Many investors hold stocks because equities have a long history, deep liquidity and a familiar role in retirement planning. Owning shares of a company is a concept most investors understand. Stocks remain a core part of many long-term portfolios for good reason.

Crypto, on the other hand, may appeal to investors who want exposure to a different kind of asset class — one that operates outside traditional equity markets and is built around blockchain-based networks rather than corporate ownership. Crypto can still be volatile. It can still be affected by regulation, interest rates, liquidity, investor sentiment and broader economic conditions. But it may offer a different source of long-term growth potential than traditional company shares.

That’s why tokenized stocks and cryptocurrencies should not be treated as interchangeable.

A stock can borrow crypto’s technology without becoming crypto. A blockchain-based trading system can make traditional assets faster to transfer without giving those assets the same characteristics as bitcoin, ether or other digital assets.

For investors, the real question is not whether stocks and crypto can use the same technology. They can.

The better question is: What kind of exposure are you actually adding to your portfolio?

If you buy a tokenized stock, you may still be buying exposure to a company. If you buy crypto, you may be buying exposure to a decentralized network, a digital asset ecosystem or the broader adoption of blockchain technology itself.

Those are different investment ideas. They come with different risks, different potential benefits and different reasons for owning them.

So if Wall Street wants crypto’s technology, that’s worth paying attention to. It suggests blockchain-based infrastructure is becoming harder for traditional finance to ignore.

But investors should not confuse the wrapper with the asset inside.

Tokenization may make stocks faster, more flexible and more convenient to trade. Crypto still serves a different role for investors who want exposure to digital assets themselves — not simply traditional assets moving on crypto-like rails.

For some investors, the answer may not be stocks or crypto. It may be understanding how each asset class could fit into a broader diversification strategy.If you realize that you’re ready to find out more about diversifying into crypto in a tax-advantaged way, get our free Crypto IRA Guide. If you already know that you’re ready to diversify into crypto, you can open your BitIRA account in just minutes.