When talking about cryptocurrency, the word “conservative” doesn’t usually leap to mind. That’s not the case for Fidelity Investments, however, which recently included the increasingly popular bitcoin spot ETFs in its Conservative All-in-One portfolio. But how do notoriously volatile cryptocurrencies fit into conservative investment strategies? It turns out, there’s more than one factor at play.

First and foremost, cryptocurrencies are inversely related to the US dollar and have a low correlation to the general market. That means that when the dollar is strong and the market is strong, cryptocurrencies may experience a dip, but when the dollar and/or the market weakens, cryptocurrencies can actually rise.

During the pandemic, many big investors saw that to be the case when Bitcoin continued to deliver returns even as other markets plummeted by 35% in five weeks. From that point forward, Bitcoin and other cryptocurrencies came to be viewed as an asset that could provide a hedge against inflation and protect wealth that would otherwise be lost to a declining market.

The emergence of Bitcoin spot ETFs earlier this year further solidified cryptocurrencies as a favored choice among investors looking to stabilize – not jeopardize – their long term portfolios. Fidelity isn’t the only one recommending to fold in Bitcoin to reduce risk, as BlackRock’s MALOX fund also includes a recommendation to invest in Bitcoin spot ETFs.

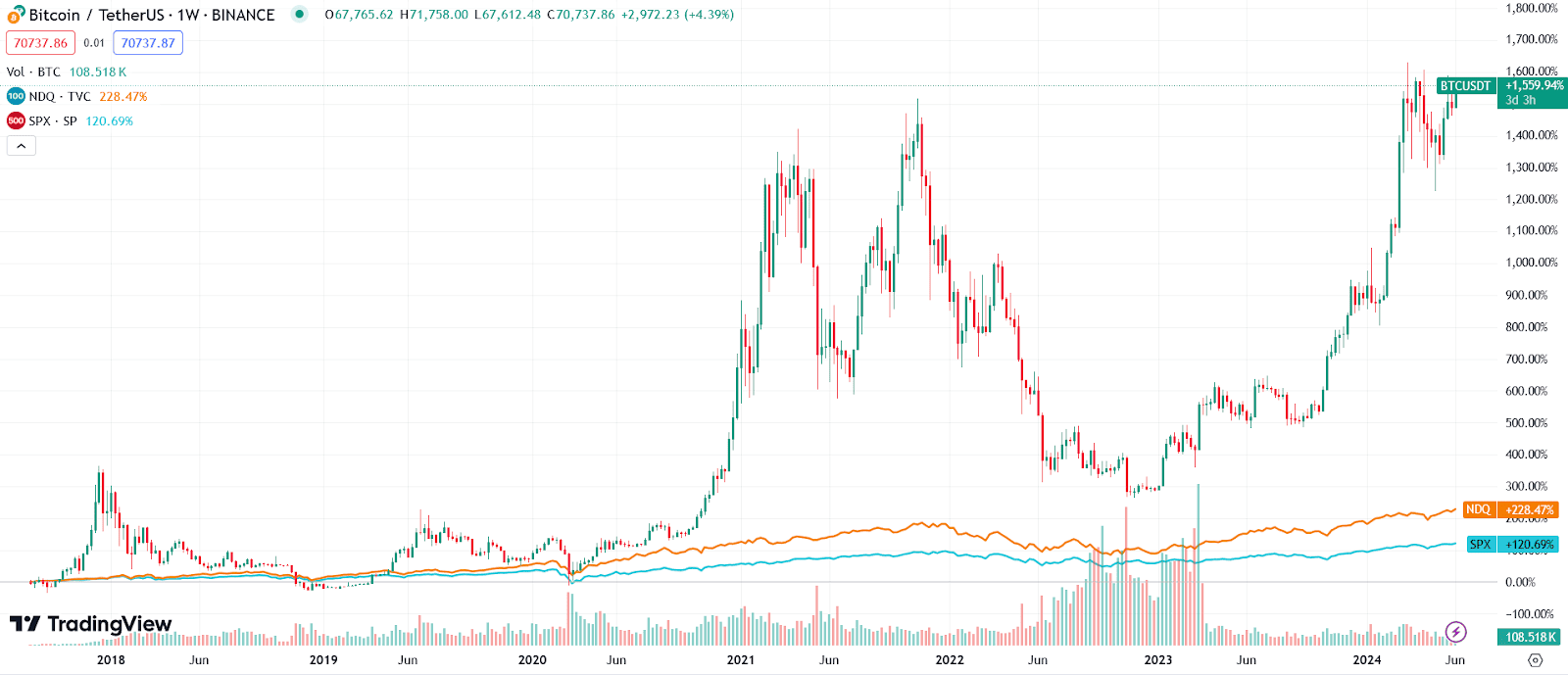

It can be confusing to hear conservative fund advisors recommending to invest in assets that have experienced – in the case of Bitcoin, at least – six drawdowns of more than 50% over a relatively short period of time. However, when pulling back and looking at the long term, it’s easy to recognize the potential value that advisors are seeing. After all, even as Bitcoin can and has fallen quickly, it can regain its value just as quickly. The chart below illustrates this, along with Bitcoin’s comparative gains to other markets.

Source: Trading View

That brings us to the second major factor that conservative advisors are looking at. Not only does cryptocurrency have a low correlation to the US dollar and the overall market, it also has the potential for significant gains, which can lend to a portfolio’s general stability. Consider the scenario where most of your assets are tied into the US dollar, and the dollar goes down. Your cryptocurrency assets could begin going up at that time – and not just a little. The degree to which your crypto investments buoy your portfolio could be sufficient to help it weather significant financial storms.

That’s not to say that conservative investors are recommending a major investment into crypto, with 1% to 3% being the recommendation in most cases. Some experts advise going as high as 5%, but not higher (as 7% proved to be too risky in test scenarios, according to Kiplinger). Many casual investors (regular people just saving up for retirement) don’t even know the breakdown of their investment portfolio. They usually rely on basic assets or whatever retirement plans their employer offers. However, everyone knows that diversification is important, so it’s probably not smart to tie up your entire 401k in a single asset class. (Speaking of which, did you know you can transfer some or all of your existing 401k to crypto?) If you’re building up your savings, make sure you’ve taken a look at your allocation percentages so you’ll know whether you’ve appropriately diversified or not. Most people probably haven’t and are leaving their heard-earned savings vulnerable to surprises in the economy!

It’s also important to recognize that these conservative investment strategies are tied to long term strategic plans rather than short term wins. Crypto will continue to be volatile in the short term, but that doesn’t change its value as a stabilizing force for your portfolio in the long term. That makes cryptocurrency an exciting and popular choice for retirement planning. Plus you can get tax advantages when you invest in a digital IRA! If that’s something of interest to you, contact us today to learn more or sign up now.